European Centre for Strategic Studies and Policy (ECSAP)

Instability in global energy markets has persisted well beyond the initial shock of Russia’s invasion of Ukraine. By 2026 Europe is far less dependent on Russian fossil fuels, yet Russia — weakened economically and politically — continues to be a source of uncertainty and risk. The invasion of Ukraine was never primarily about oil and gas, but the conflict accelerated shifts in global energy markets that will shape the decade ahead.

What is happening now (2026)

By early 2025, the physical flow of oil and gas from Russia to Europe has dropped to a fraction of pre-war levels. Europe has largely replaced Russian oil with supplies from the Middle East, Africa, and the United States. Gas imports from Russia have fallen by more than two-thirds, offset in part by LNG shipments from Qatar, the US, and new suppliers in North and East Africa.

Prices remain volatile. Natural gas prices in Europe are still well above their pre-2022 averages, though lower than the extreme spikes of 2022–2023. Oil has stabilised somewhat, but OPEC’s production decisions, combined with geopolitical tensions in the Middle East, keep the market on edge.

Europe’s consumers continue to feel the pressure of high energy costs, which remain a driver of inflation and cost-of-living pressures. Energy security has become a central theme in national debates and in EU policymaking.

The next year (2026–2027)

Through the rest of 2026 and into 2027, Europe will consolidate its new network of long-term supply contracts. Germany, Italy, and other previously gas-dependent states are now tied into deals with Qatar, Algeria, Norway, and the United States. Floating LNG terminals around the North Sea and the Mediterranean are fully operational, locking Europe into a new pattern of dependence — one more diversified, but not necessarily cheaper.

NATO has incorporated energy security more explicitly into its agenda. The alliance now views stable access to affordable energy as part of its collective defence, particularly as Russia continues to use energy flows as leverage against countries seen as unfriendly to its interests. A loose “energy NATO” is emerging, linking Western importers with a group of exporters across the Middle East, the Caspian, and Africa.

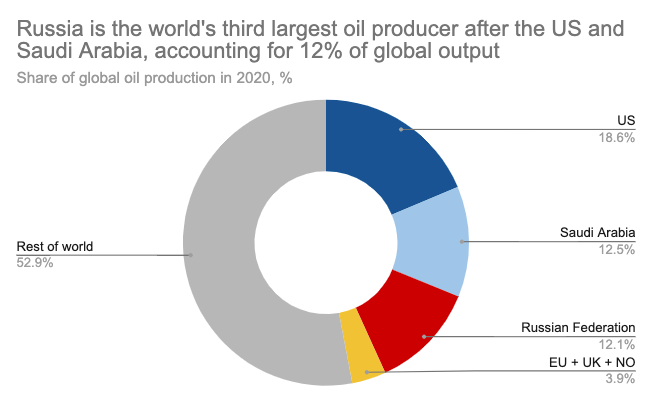

It’s the world’s 2nd largest gas producer after the US, responsible for 17% of global output in 2020. It’s also the world’s 3rd largest oil producer after US / Saudi Arabia, responsible for 12% of output in 2020.

Looking further ahead (2027–2028)

By 2027 or 2028, several major projects launched after the Ukraine war — from Eastern Mediterranean gas to expanded US LNG capacity — should be delivering new volumes to global markets. Europe will have advanced further in renewables and electrification, particularly in heating and transport. The Ukraine war, in retrospect, will be seen as having accelerated Europe’s transition to a lower-carbon economy.

But instability will persist. Global energy demand continues to rise, driven by population growth and economic development across Asia and Africa. Oil, gas, and coal still dominate the global mix. Climate commitments remain behind schedule, and extreme weather events are already putting further stress on fragile regions.

Russia, cut off from Western capital and technology, has seen its oil and gas production decline steadily. Some new pipelines to China are operating, but Beijing remains cautious about over-reliance on Moscow, balancing imports with supplies from Central Asia and the Gulf. Russia’s reduced revenues have weakened its economy but not eliminated its ability to destabilise its neighbours.

Conclusion

As of 2025, the global energy market is more diversified than in 2022, but not more stable. Europe is no longer beholden to Russia’s energy dominance, yet high prices, volatility, and the geopolitics of supply continue to shape policy. An impoverished Russia remains unpredictable, while the climate crisis ensures that the world’s long-term energy insecurity is far from resolved.

Russia-Ukraine conflict gives rise to global risk exposure in capital flows, trade, commodity markets

Geopolitical tensions between NATO and Russia have been high for some time. Russia’s invasion of Ukraine has NATO-Russia-relations at their most precarious since the cold war. The Russian invasion of Ukraine has not only initiated a global humanitarian crisis, it’s given rise to greater risk exposures in capital flows, trade and commodity markets worldwide.